The announced merger between Optus Financial, M&F Bancorp marks one of the most significant developments in minority banking in decades. Announced on July 22, 2026, the transaction exceeds $105 million. It will create the largest Black-owned bank in the United States. The bank will have approximately $1.27 billion in assets, subject to regulatory and shareholder approval.

Scale matters in banking. Larger balance sheets allow institutions to make larger loans, invest in technology, attract deposits, and expand access to capital in underserved communities. The combined institution strengthens the Minority Depository Institution (MDI) sector while preserving a mission-driven focus on financial inclusion.

The merger reduces the number of Black-owned banks by one. Consequently, it increases the scale and competitive capacity of the resulting institution. The transaction illustrates an important trend: strategic consolidation can strengthen minority banking while maintaining community development objectives.

We are proud to serve as a Supporting Organization for The Economist’s 2026 General Counsel Summit series, bringing together leading general counsel, chief legal officers, corporate executives, and legal innovators from around the world.

General Counsel Summit US September 15, 2026 | New York City. Explore how legal leaders are responding to an increasingly unpredictable legal and business environment, where the most important decisions extend beyond the practice of law into corporate strategy and enterprise risk management.

General Counsel Summit Asia October 15, 2026 | Singapore

Join senior legal executives from across Asia-Pacific to discuss geopolitical risk, AI governance, cross-border regulation, cybersecurity, ESG, M&A, and the evolving role of the modern general counsel in one of the world’s fastest-changing business environments.

General Counsel Summit UK November 12, 2026 | London The 23rd annual summit convenes more than 600 general counsel and chief legal officers to examine how legal leadership is adapting to AI, regulatory change, employment law reform, geopolitical uncertainty, and increasingly complex corporate governance challenges.

The June 2026 Employment Situation Report presents a familiar challenge for policymakers and investors: a lower unemployment rate that masks a weakening labor market. While the official unemployment rate declined to 4.2%, the underlying data point to slowing employment growth, declining labor force participation, and persistent racial disparities that continue to place Black workers and minority-owned businesses at elevated risk. Our analysis of the May report argued that headline numbers were overstating labor-market strength. The June data reinforce that conclusion.

A Lower Unemployment Rate for the Wrong Reason

On its face, the June report appears encouraging. Unemployment declined from May, suggesting continued resilience. A closer examination tells a different story.

Payroll employment slowed significantly. Previous months were revised downward. Most importantly, labor force participation declined, meaning part of the reduction in unemployment occurred because workers stopped looking for work rather than because employers dramatically increased hiring.

A falling unemployment rate driven by declining labor force participation is fundamentally different from one driven by robust job creation. The former reflects weakening labor demand and growing discouragement among workers.

Black Workers Continue to Bear the Burden

The June report again demonstrates that labor-market weakness is not evenly distributed.

Black unemployment was unchanged from last month’s 6.6%, still more than 90 percent higher than the White unemployment rate of 3.6%.

Hispanic unemployment: 5.2%

Asian unemployment: 3.9%

Black women: 5.7%

These differences represent millions of households experiencing very different economic realities despite living in the same national economy. While unemployment changed only modestly for most demographic groups between March and June, Black workers continue to experience substantially higher unemployment than virtually every other major labor-market group.

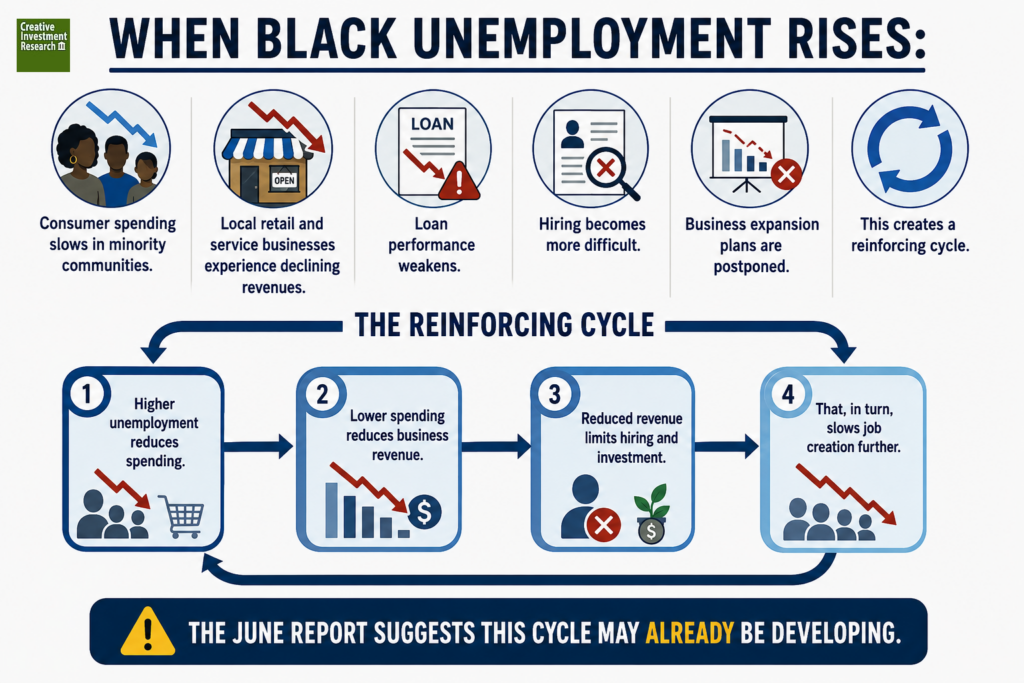

Why This Matters for Minority-Owned Businesses

Minority-owned firms are uniquely sensitive to labor-market conditions because many operate in industries that depend heavily on local consumer demand, neighborhood employment, and small-business lending.

When Black unemployment rises:

Consumer spending slows in minority communities.

Local retail and service businesses experience declining revenues.

Loan performance weakens.

Hiring becomes more difficult.

Business expansion plans are postponed.

This creates a reinforcing cycle.

Higher unemployment reduces spending.

Lower spending reduces business revenue.

Reduced revenue limits hiring and investment.

That, in turn, slows job creation further.

The June report suggests this cycle may already be developing.

The AI Transition Is Beginning to Show Up

Another important development is the interaction between slowing employment and ongoing artificial intelligence adoption. Businesses continue restructuring workforces while simultaneously confronting:

elevated interest rates,

persistent inflation,

federal fiscal uncertainty,

geopolitical instability, and

rapidly expanding AI deployment.

Historically, technological transitions create opportunities over the long term while generating short-term labor dislocation.

Minority workers and minority-owned businesses often experience these adjustment costs first because they typically possess fewer financial reserves and less access to affordable capital.

Without deliberate investment in workforce development, digital infrastructure, and access to capital, AI-driven productivity gains risk widening existing economic disparities.

Looking Beyond the Headlines

Investors should pay closer attention to the underlying trends:

slowing payroll growth,

downward revisions to previous employment gains,

declining labor force participation,

persistent racial employment gaps, and

weakening momentum in overall hiring.

Taken together, these indicators suggest that the labor market is cooling more rapidly than the headline unemployment rate implies.

Policy Implications

The June employment report reinforces several priorities. Policymakers should avoid relying solely on the national unemployment rate when assessing labor-market conditions.

Support for minority-owned businesses becomes increasingly important during periods of labor-market deceleration. Access to capital, procurement opportunities, and workforce development programs can help prevent temporary labor-market weakness from becoming long-term economic decline.

Bottom Line

The June employment report should not be interpreted as evidence that the labor market has regained strength.

Instead, it signals a labor market that is gradually losing momentum while continuing to distribute economic pain unevenly across demographic groups.

For Black workers, minority-owned businesses, and the communities they support, the data suggest that the second half of 2026 may become increasingly challenging unless employment growth accelerates and labor force participation stabilizes.

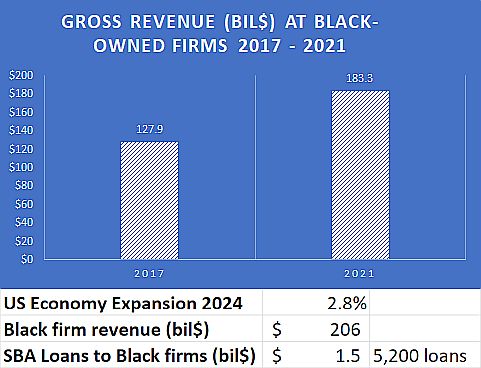

The U.S. economy experienced a 2.3% annual growth rate in the fourth quarter of 2024, culminating in a 2.8% expansion for the entire year. This growth was primarily driven by robust consumer spending and increased government expenditures. See: https://www.impactinvesting.online/2025/01/economic-growth-in-2024-assessing.html

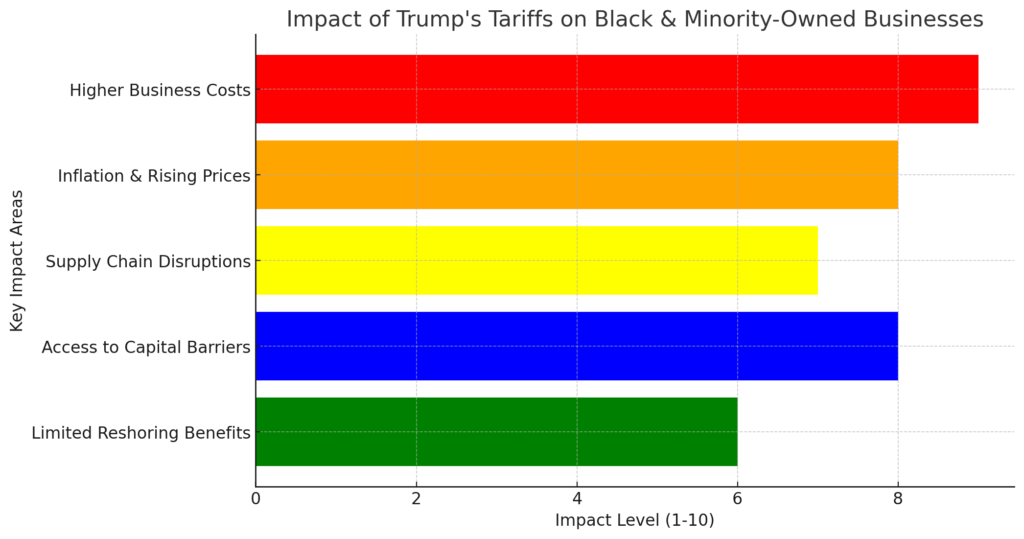

The impact of Trump’s proposed tariffs on Black and minority-owned businesses could be significant and largely negative, given their reliance on cost-effective supply chains, imported goods, and price-sensitive consumers. Here’s a breakdown of how these tariffs might affect minority businesses: https://www.impactinvesting.online/2025/02/trumps-tariffs-heavy-blow-to-black-and.html

The lawsuit filed by Andav Capital and its founder, Nisha Desai, against PayPal represents not only a fundamental misunderstanding of the purpose and legality of diversity initiatives but also a bad-faith attempt to weaponize civil rights law against efforts to address historical and systemic inequities. See: https://www.linkedin.com/pulse/response-paypal-minority-vc-funding-lawsuit-zbqse/

NEW YORK, Dec. 13, 2024 — Dream Chasers Capital Group LLC (“Dream Chasers”) is raising serious concerns about irregularities during the Carver Bancorp, Inc. (“Carver,” or the “Company”) (NASDAQ: CARV) Annual Meeting of Shareholders held on December 12, 2024. Dream Chasers is urging Carver’s Chief Executive Officer, Donald Felix, and the Board of Directors to deliver clarity, transparency, and accountability to shareholders after a contentious meeting.

Preliminary results reveal that approximately 70% of retail shareholders supported Jeffrey “Jeff” Anderson and Jeffrey Bailey for election to the Board. However, these results were clouded by unexpected procedural decisions, including an unexplained 45-minute extension of voting, despite the voting deadline being set weeks in advance through Carver’s definitive proxy filing with the SEC on October 31, 2024.

Dream Chasers has formally communicated its concerns to Carver’s leadership in a letter detailing several demands to ensure fairness and transparency in the election process.